Budgeting Course

I do want you to know that you can learn to manage money wisely and live a much more peaceful and fruitful life. My hope for you is that this budget course will bless you and allow you to learn how to manage your money so that it doesn’t manage you. In order to feel at peace regarding your personal finances, you can’t put off today what needs to be done until tomorrow.

Friend, please make getting organized from a personal financial planning standpoint a priority in your life from this moment forward. Then you can live a more peaceful and fruitful life.

“Come to me, all you who are weary and burdened, and I will give you rest.” (Matthew 11:28 NIV)

“If any of you lacks wisdom, you should ask God, who gives generously to all without finding fault, and it will be given to you. But when you ask, you must believe and not doubt, because the one who doubts is like a wave of the sea, blown and tossed by the wind.” (James 1:5-6 NIV)

1.

dream

TAKE A MOMENT TO Think ABOUT YOUR HOPES

Make a list of your financial dreams, goals, and hopes for the future. If you’re married, include your spouse in this discussion. There are no wrong answers. The only way you can fail is if you never start dreaming and making plans to achieve your goals!

Let this take some time. Think and dream about what you want your life to look like in the future.

Tip: Keep this list somewhere you can see it often! THIS LIST will inspire you on days you’re feeling less motivated.

2.

Track Expenses

Do you know how much money you spend each month? If not, do not be embarrassed. Let’s figure it out together.

I suggest going to an all cash system for a couple of months to track your expenses. If you are very disciplined, you can use a shoebox and save every single receipt for a month. Do not leave anything off of your list. Put the shoebox next to the door of your home. Then empty your receipts from your purse or wallet every time you come home. If you spend $4.50 at your local coffee shop, then save the receipt. This is the only way to truly know how much money you are spending each month. After this, you will be able to determine how much discretionary income* you have.

Be prepared to be surprised. Many people are shocked to find out how much money they spend on miscellaneous items like lattes, dining out, shopping, or entertainment. None of these expenses are bad. You just need to make sure you are spending less than your make. The goal is to have money left over each month to allocate towards your savings goals.

*Discretionary income is the amount of money you can afford to save each month after all of your expenses are paid.

3.

monthly budget

Detailed & Realistic

I want to encourage you to see creating a budget as a way to be responsible and respectful of the resources that God has entrusted you. What you give attention to in your life is what you will gain affection for. What you have affection for changes your activities and attitude. If you truly love God and want to show affection for him, one of the ways to do that is to actively and responsibly manage your personal finances.

"For where your treasure is, there your heart will be also." (Matthew 6:21 NIV)

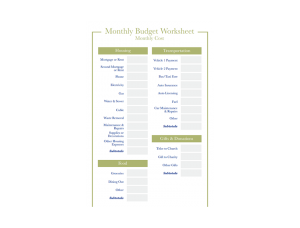

The biggest objection I hear related to creating a monthly budget is not knowing where to start. In order to eliminate any and all objections, I’ve done the heavy lifting for you because I believe this is so important. Use the budget worksheet below to get started on your monthly plan.

Suggested Budget Percentages According to Budget Categories

In order for a budget to actually work and benefit your family, it has to be tailored to your unique lifestyle and situation. I have included two resources that give realistic suggestions on how to begin your budgeting process by category.

The first suggestion source is The Total Money Makeover by Dave Ramsey. The second suggested source is Money Matters by Larry Burkett.

4.

reducing expenses

Discover opportunities

After carefully reviewing your budget, identify which expenses you regularly incur that are unnecessary. For example, eating out in restaurants or going to the movies are not necessary for your daily survival. These are called discretionary expenses. Remember, these activities are not bad, you just don’t need these activities in order to survive.

Try to think of ways to entertain yourself without spending money

- go for a walk

- visit public parks

- enjoy local playgrounds

- attend activities at your local church

- read a library book

- call a friend

- get creative

Once your discretionary expenses have been identified, try to forgo as many of these expenses as possible. Use the money you would have spent on discretionary expenses to start funding a cash reserve account.

5.

Inventory

Of current Possessions

Do you own anything you no longer need, use, or want that could be valuable to someone else? You may be able to clean out some clutter in your home and turn it into cash. Simplifying is a great way to get your home more organized and start funding your cash reserve account. It will be a double blessing to you and your family.

"But remember the Lord your God, for it is he who gives you the ability to produce wealth, and so confirms his covenant, which he swore to your ancestors, as it is today." (Deuteronomy 8:8 NIV)

Here are a few easy ways to make a little extra cash:

- Clean out your home and have a garage sale. Invite friends and family members to participate.

- Sell good quality clothes to a resale shop

- If you have children, do you have any baby gear, toys, or clothing that your children have outgrown? Many communities have large swap meets for children’s items that are used, but still in very good condition.

Of course, there are many more things you can do to de-clutter and raise some extra cash. Once again, be creative.

6.

Emergency Savings

Start building a cash reserve

One of the greatest stressors in America regarding personal finances is living over-extended. This is one of the reasons that credit cards were invented. People who live paycheck to paycheck, never quite get ahead because they do not have a cash reserve account. A cash reserve account is money you need to have on hand to pay for unforeseen expenses. I can promise you this: you are not in control. Things will break; people will get sick; and disasters will happen. If your refrigerator suddenly breaks, or you receive a very large unexpected medical bill, life will be very stressful without any cash to fall back on to pay for these expenses.

Rest assured, it’s not all bad news. You absolutely can plan for these types of events in advance. If you have savings on hand, then life will become much less stressful. There is a lot of truth in the old saying, “Everything in life is easier with a little cash.”

My prayer for you is that you will be encouraged and inspired to build up and maintain a cash reserve account. I do not ever want you, my friend, to be one flat tire or other unforeseen expense, away from being flat broke. I want you to be protected from financial hardships in the future by being proactive with your finances.

save 3 Months of Living Expenses

Continue to save your discretionary income until you have at least three months worth of living expenses in your new savings account. This new savings account is now earmarked for emergencies only. This is not a rainy day fund to use if you suddenly have a desire to take a vacation or buy a boat. After you have three months of cash in your savings account, don’t stop saving. You have now become much more disciplined in managing your monthly budget. Most likely, you have not even missed the funds you have been saving each month.

Unstable Income?

If you are uncertain about whether or not your job is stable, then consider setting aside six months worth of living expenses. This is also a good benchmark for people who are self-employed, or executives who work on commission only. If your income fluctuates from month to month, you will be better prepared financially to handle any swings in your income if you have adequate cash on hand.

Open A Separate Bank Account

I recommend opening a savings account at your local bank that is separate from your regular checking account so the funds don’t comingle. Why? Because it is very tempting to spend extra cash that sits in your regular checking account.

7.

Relax

& ENJOY your new financial freedom in regards to unforeseen expenses

It’s much easier to reach goals incrementally over time, if you have a strategic plan in place and commit to follow it. Take a moment to enjoy that you’ve taken some great steps in your financial wellness!